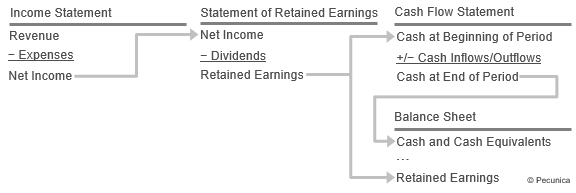

The cash flow statement identifies the cash that flows into and out of the company during the reporting period compliments the income statement and balance sheet. While accrual basis of accounting is generally used for the balance sheet and income statement, the cash flow statement uses cash basis accounting. Where a company accrues accounting revenues, it may not actually receive the cash, which could produce profits and taxes payable but not provide sufficient liquidity to remain solvent.

| Cash Flow through the Financal Statements |

Source:

|

If cash from operating activities is regularly greater than net income, the company’s earnings are “high quality”. If cash from operating activities is less than net income, an analysis should reveal why net income is not being transformed into cash.

Investments in noncurrent assets is necessary for the replacement and expansion of a company’s productive capacity. Where the investing cash flow over succeeding periods is positive, the firm’s ability to grow and continuation as a going concern may be called into question. If the company regularly generates more cash than it is uses, it will be able to increase dividends, buy back stock, reduce debt or undertake investments.

Financing cash flow is reflected in the changes in the company’s short-term borrowings, long-term debt and owners’ equity. Where an increase in borrowings or paid-in capital shows a cash inflow, a decrease in the account balances results from loans being paid off, bond retirement or stock redemption.

Leave A Comment

You must be logged in to post a comment.