A tranched ABS issued by a special purpose vehicle (SPV) that is backed by a pool of receivables structured into multiple tranches, each having different rights over the portfolio of assets and risk-return profile, is a collateralized debt obligation (CDO). A CDO is distinguished from an asset-backed security (ABS) comprising one class of security, all of which have the same rights and risk-return profile.

A cash collateralized debt obligation is a structured pay-through security created by a SPV that buys an originator’s receivables or other financial assets that serves as collateral and that are ordered into multiple tranches (classes) by seniority and/or repayment time, with each tranche sold as a separate security with different rights over the portfolio. A CDO is a type of structured asset-backed security (ABS).

| The Structure of a CDO (Example) | ||||||

| Rating | Tranche | 5-Year EL |

Multiplier | Protection Value |

Size | Spread (bps) |

| Aaa | 8-100% | 0.07% | 16.8 | 1.21% | 92% | 26 |

| Baa | 0-100% | 1.30% | 5.1 | 6.61% | 100% | 144 |

| Ba | 4-8% | 6.70% | 2.1 | 14.07% | 4% | 321 |

| Caa | 0-4% | 36.50% | 1.3 | 47.45% | 4% | 1376 |

A collateral mortgage obligation (CMO) is an example of a pay-through security. For a CMO, pass-through mortgage-backed securities (MBOs) or mortgage loans are grouped together to serve as collateral for the pay-through CMOs, the pool of MBOs is divided into senior and junior tranches, and the senior tranches are then subdivided into different credit and prepayment risk tranches, in order to meet the specific risk/reward needs of various investors.

Whereas CMOs only contain mortgages, CDOs contain a range of loans such as car loans, credit cards, commercial loans and even mortgages. CDOs and CMOs are pass-through securities, as opposed to ABS and MBS pay-through securities.

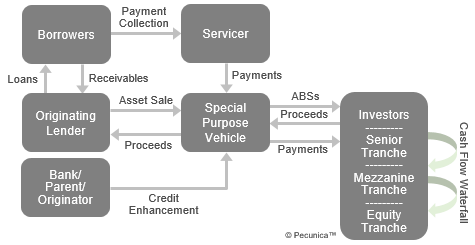

With a pay-through security, the payments received on the underlying debt obligations by the SPV are first used to make payment to the senior tranches and then for payment to the more junior tranches only when the priority claims of each more senior tranche are satisfied (the “cashflow waterfall”).

| Asset Securitization Structure of a Pay-Through Security |

Source:

|

The cash flows from the pool of assets are not passed on directly to investors, but are first restructured by the SPV, which smooths the flows and allows the cashflows to be directed to the different tranches – different classes with different rights. If default on any of the assets occurs, the tranches are impaired in order of increasing seniority.

Leave A Comment

You must be logged in to post a comment.