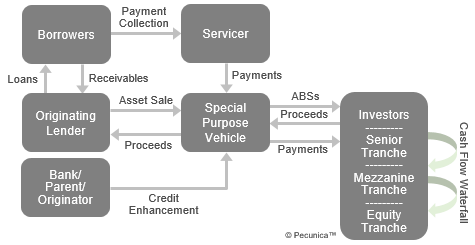

An asset-backed security (ABS) is a marketable security that is issued by a special purpose vehicle (SPV) that buys financial receivables, such as automotive leases and mortgage loans, that serve as collateral for and to generate the interest and principal payments on the issued securities. A tranched ABS issued by a special purpose vehicle (SPV) that is backed by a pool of receivables structured into multiple tranches, each having a different seniority and risk-return profile, is a collateralized debt obligation (CDO), as distinguished from an ABS comprising one class of security, all of which have the same rights and risk-return profile.

The risks of an ABS, including credit, interest-rate and prepayment risks, are directly connected with the asset pool and the structuring of the securities. The pooled assets are the only assets of the SPV and, as nonrecourse financing, the debtors in respect of the underlying assets in an ABS – not the originator – are held responsible for the assets and the performance of the securities.

| Asset Securitization Structure and Flow Process |

Source:

|

The major stages in the ABS structuring process are:

- Establishment of a bankruptcy-remote third-party securitization vehicle (SPV), generally by the lease originator;

- Packaging and sale of legal title to and all rights under the leased assets on a nonrecourse basis by the originator to the SPV;

- Addition of credit enhancement to improve the credit rating and marketability of the security; and

- Creation and sale of the ABS secured by the pooled assets held by the SPV.

Lease receivables from various forms of equipment leasing (e.g., automobile, aircraft and railcar leases) as well as real estate leases lend themselves to securitization. Independent lessors and captive finance companies are the most active users of the ABS market for funding.

Leave A Comment

You must be logged in to post a comment.