A type of reorganization based on US Chapter 11 procedures is a Chapter 11-style reorganization. A Chapter 11-style reorganization is a distressed-debt restructuring in which an insolvent firm’s incumbent management remains in control of the company and is responsible for managing the firm during the insolvency proceedings and carrying out the duties of an administrator. As with compositions, an automatic stay freezes creditors’ positions at the time of the bankruptcy filing and negotiations among stakeholders are conducted with the aim of achieving a court-approved plan.

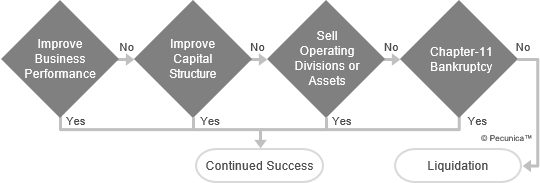

| Decisions in Distressed Firm Scenarios |

Source:

|

Prepackaged bankruptcy is a hybrid form of distressed-debt restructuring that combines the features of both traditional Chapter 11-style reorganization and out-of-court restructuring, where the debtor negotiates a plan of reorganization with significant creditors before filing for bankruptcy. Firms resolving financial distress through a prepackaged bankruptcy file the plan at the same time as their Chapter 11 bankruptcy petition. The plan needs a confirming vote by two-thirds of voting creditors in amount and more than 50 percent in number from each class of creditors. DIP financing may be provided in a prepackaged bankruptcy where an asset-based lender supplies the funds to work out an up-front settlement with creditors.

| Reasons for Higher Recovery of Prepackaged Chapter 11s |

| 1. Reorganization is negotiated out-of-court, requiring much less time than traditional Chapter 11 restructurings. |

| 2. Prepetition negotiation and agreement result in lower legal costs, shorter time in bankruptcy, and fewer bargaining frictions between shareholders and creditors. |

| 3. Firms that adopt prepackaged restructurings tend to be more operationally sound. |

An administration is an insolvency procedure under the insolvency laws of such common law jurisdictions as Australia, Canada, Ireland and the United Kingdom in which an administrator is appointed to restructure a financially distressed firm in order for it to continue as a going concern, to protect the firm from its creditors, and to achieve a better outcome for creditors than through liquidation. In contrast to US Chapter 11, where the insolvent firm’s incumbent management remains in control throughout the restructuring process, an administrator is appointed to manage the company’s affairs in order to protect the interests of the creditors of the insolvent company and to balance their respective interests.

Leave A Comment

You must be logged in to post a comment.