A money market fund (MMF) comprises a portfolio of high-quality, short-term securities, such as treasury bills and commercial paper, and that pays dividends that normally reflect short-term interest rates. They are managed with the objective of maintaining a highly stable asset value through liquid investments, while paying interest income to investors.

As with bond funds, US money market funds are classified by their principal underlying assets:

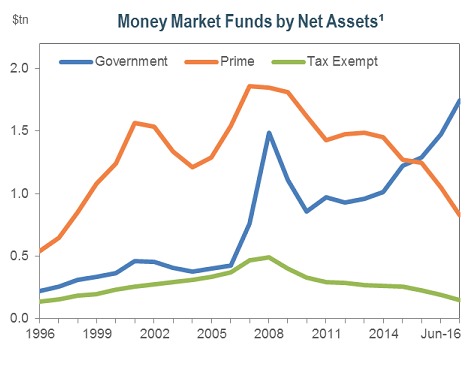

- Government money market fund – 99.5% or more of its total assets in cash, government securities, and/or repurchase agreements that are fully collateralized by government securities or cash.

- Tax-exempt money market fund – Comprised of the short-term debt securities of state and local jurisdictions (municipal notes), which are usually exempt from US federal income tax and the income tax of the state of issue.

- Prime money market fund – Mainly high-quality commercial paper, certificates of deposit and short-term government, [donotmark]agency[/donotmark] and municipal securities.

| Impact of SEC Regulation Change on MMFs in 2016 |

Source:

|

Money market funds are also characterized by the nature of investor they are targeted to:

- Retail money market fund – Offered primarily to retail investors, with policies and procedures designed in the [donotmark]interest[/donotmark] of such investors; and

- Institutional money market fund – Requiring a high minimum investment and marketed to corporations, governments and financial fiduciaries, commonly set up to automatically [donotmark]pool[/donotmark] idle cash from the main operating accounts of the institutional investors and to [donotmark]transfer[/donotmark] (“sweep”) the cash to the fund overnight.

Money market funds seek to limit losses due to [glossary_mark id="57040"]credit[/glossary_mark], [glossary_mark id="71277"]market[/glossary_mark] and liquidity risks. They are commonly used to provide liquidity and for principal preservation.