Debt can be contractually and/or structurally subordinated. Subordination is usually contractual and is essentially the purpose of intercreditor and subordination agreements. Contractual subordination is a contractual arrangement under which the rights and remedies of a first-lien lender are free from any actions of a second-lien lender with respect to the common debtor (and often any guarantor) and the shared collateral.

A subordination agreement is an arrangement under which a current lender contractually undertakes to subordinate some or all of its rights against a borrower to the rights and interests of another lender. It establishes that a lender’s security interest in collateral, though obtained later, will be senior to the current lender’s security interest in that collateral. The subordination agreement:

- Establishes the relative priority of the claims of the lenders to security;

- Prohibits or restricts payments to the junior lender; and

- Prohibits or restricts the right of junior lenders to foreclose on the collateral or exercise any other default remedies until senior lenders have been paid in full.

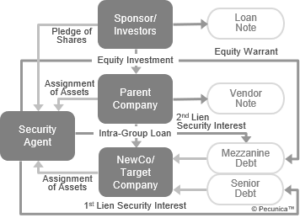

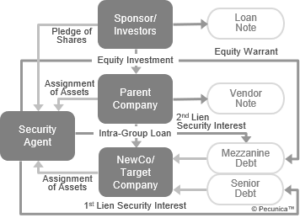

Structural subordination is the subordination by virtue of the company group structure, where indebtedness incurred at the parent or holding levels in a commercial group to debt incurred at the subsidiary level. The subsidiary-level creditors have first claim to the subsidiary assets while parent-level creditors are limited to a claim on the assets of the parent company, which typically consists only of equity in the subsidiary.

If the parent company in a special-purpose vehicle (SPV) is set up exclusively for the financing, its revenues consist substantially or wholly of dividends on equity or payments on downstream loans since it has no operating revenues of its own. If the operating subsidiary makes no distribution to the holding company, no funds may be available to the parent company to pay the lender.

| Acquisition Finance Flows |

Source:

|

Leave A Comment

You must be logged in to post a comment.