That portion of outstanding loans and leases that is deemed to be uncollectible is charged off and reported as an allowance for loan and lease losses at the end of the accounting period. The allowance for loan and lease losses (ALLL) is the asset contra asset used for crediting and accumulating estimated amounts of loans and leases that will not be collected, it reducing the carrying amount of loans and lease receivables by the amount charged (provisioned) against earnings to absorb impairment losses. No allowance is recognized for loans and leases held for sale because they are reported at the lower of cost or fair market value.

| Lessor Recognition of Increase in ALLL | ||||

|---|---|---|---|---|

| Date | Provision for Loan and Lease Losses | xxxx | ||

| Allowance for Loan and Lease Losses | xxxx | |||

| To record an increase in uncollectible loans and leases | ||||

When a loan or a lease is deemed uncollectible, the balance is charged-off and the ALLL is reduced by the same amount. Net charge-off (NCO) is the total allowance for loan and lease losses (ALLL) for the period less recovery of any amounts charged off in previous periods. The provision for loan and lease losses (PLLL) is an income statement expense account reflecting adjustments to the ALLL for any deficiency or surplus resulting from an increase or decrease, respectively, in credit losses in that year. PLLL is the amount required to maintain the ALLL at a level that, in management’s judgment, is sufficient to absorb losses in the loan and lease portfolio. In those periods when the ALLL is determined to exceed the PLLL, a credit is recorded to the ALLL. The PLLL is usually a major expense for most financial institutions.

NCO = ALLL - Recovery of Previous Charge-Offs

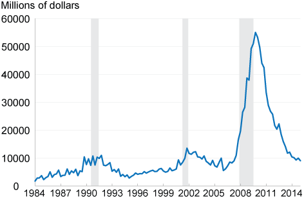

| Net Charge-Offs* 1984-2014 |

Source:

|

| Source: Cleveland Fed |

Leave A Comment

You must be logged in to post a comment.