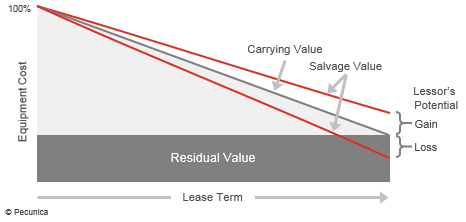

The commercial value of a leased asset under a finance lease at lease termination as set at lease inception equal to the estimated net proceeds from the asset’s sale, its remarketing or payments from its re-lease for fair value at the end of the lease term is its residual value (RV). A leased asset’s residual value, if any, is equal to its remaining carrying value after it has been fully depreciated at the end of its lease term.

The residual value of a lease can be guaranteed or unguaranteed. Generally, the owner of the leased asset for tax purposes bears the lease residual value risk.

| Lessor Cash Flows | |||

|---|---|---|---|

| Period | 1 | 2 | n |

| Cash Flow | Rental Payment ↑ | Rental Payment ↑ | Rental Payment ↑ |

| ↓ Investment | Residual Value ↑ | ||

In contrast to residual value, salvage value is the value that can be actually realized by a lessor once a leased asset has been reacquired at the end of the lease term. Salvage value is an asset’s realizable value equal to the net sale proceeds from the leased asset’s remarketing and sale or the rental payments from its re-lease. It is frequently agreed that if the asset’s salvage value is more than its residual value the lessee receives the difference.

| Lease Salvage Value |

Source:

|

Leave A Comment

You must be logged in to post a comment.