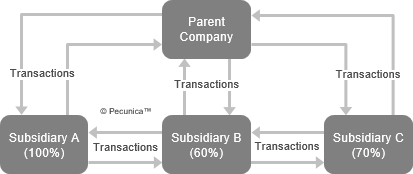

An intercompany transaction is a transaction between affiliated companies (i.e., between a parent company and one of its subsidiaries or between a parent’s subsidiaries). The transactions between the members of a company group must be considered and eliminated for the consolidation of affiliates.

| Intercompany Transactions |

Source:

|

An intercompany elimination is a cancellation of intercompany balances and transactions when preparing consolidated statements, whereby assets and liabilities transferred within the company group must be returned to their initial book value and intercompany gains or losses must be eliminated from the consolidated statements using either a consolidated worksheet or an elimination ledger.

Any transaction between affiliates of a company group requires elimination, including:

- Elimination of equity in company acquisitions – When one company acquires another company, only the acquirer’s share of the shareholders’ equity of the acquired company is eliminated through consolidation in the equity section of the consolidated financial statements.

- Unrealized gain in ending inventory due to intercompany sale of above-cost inventory not later sold to third parties prior to year-end.

- Unrealized gain due to intercompany sales of fixed assets above net book value – Such sales are only internal transfers of assets and no gain or loss should be recognized.

- Elimination of intercompany profits – Any intercompany profit or loss on assets remaining within the group must be eliminated and only profits and losses from third-party transactions should be included in the consolidated statements.

- Intercompany loans – When one group company makes a loan to another affiliated company, there are several items that have to be eliminated on both sides:

- Loans receivable and loans payable;

- Interest income and interest expense; and

- Interest payable and interest receivable.

Leave A Comment

You must be logged in to post a comment.